Non-Resident Indians (NRIs) need bank accounts to manage income earned in India and abroad. Banks offer two options—Non-Resident External (NRE) and Non-Resident Ordinary (NRO) accounts. An NRE account is suited for holding foreign earnings, while an NRO account helps manage income from India. These accounts differ in taxation, repatriation rules, and deposit sources. Knowing their features and differences could help NRIs choose the right option based on their financial needs.

What Is an NRE Account

An NRE (Non-Resident External) account is a savings tool designed for NRIs to hold and manage foreign earnings in India. Deposited funds must originate from abroad and will be held in Indian Rupees (INR). Both the principal and interest are fully repatriable, allowing easy transfer of funds overseas. Interest earned is tax-free in India.

This account is ideal for NRIs looking to save in India while avoiding Indian income tax liabilities.

Features of an NRE Account

An NRE account offers several benefits for NRIs looking to manage foreign earnings in India. Here are its key features:

Currency

The account balance is held in Indian Rupees (INR).

Deposit Source

Only foreign earnings can be deposited into the account.

Repatriation

Both the principal amount and interest earned are fully repatriable.

Taxation

Interest earned on deposits is exempt from Indian income tax.

Usage

The account can be used for investments, remittances, and payments in India.

What Is an NRO Account

An NRO (Non-Resident Ordinary) account helps NRIs manage income generated in India, including rent, dividends, and pensions. It accepts deposits in both foreign and Indian currencies, but the balance is held in Indian Rupees (INR). Repatriation is limited and requires tax compliance. The interest earned is taxable in India. This account is suitable for NRIs who need to handle financial activities within India.

Features of an NRO Account

An NRO account helps NRIs manage income generated in India. Here are its key features:

Currency

Funds are maintained in Indian Rupees (INR).

Deposit Source

Accepts deposits from both foreign earnings and Indian income sources.

Repatriation

Limited repatriation is allowed after applicable tax payments.

Taxation

Interest earned on the account balance is subject to Indian income tax.

Usage

Suitable for handling income from rent, dividends, pensions, and other Indian earnings.

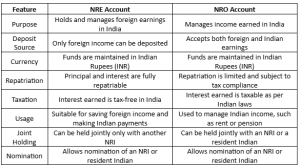

Key Differences Between NRE and NRO Accounts

NRE and NRO accounts serve different purposes for NRIs, mainly based on the source of funds, taxation, and repatriation rules. While an NRE account is used to hold foreign earnings, an NRO account helps manage income earned in India. Below is a detailed comparison of their features:

Tax Implications of NRE and NRO Accounts

The tax treatment of NRE and NRO accounts differs significantly. While an NRE account offers tax benefits, an NRO account is subject to taxation in India. Here are the details:

NRE Account

The principal and interest earned on an NRE account are fully exempt from Indian income tax. This makes it beneficial for NRIs who want to hold and manage foreign earnings in India without tax liabilities. Since there is no tax deducted at source (TDS), the entire interest amount remains available to the account holder.

NRO Account

Interest earned on an NRO account is subject to taxation in India as per the Income Tax Act, 1961. Tax Deducted at Source (TDS) is applied at rates specified by Indian tax authorities. NRIs can claim tax benefits under ‘Double Taxation Avoidance Agreements’ (DTAA) if applicable, reducing overall tax liability.

Fund Repatriation Rules

Repatriation refers to the transfer of funds from an Indian account to a foreign country. NRE and NRO accounts have different repatriation rules, affecting how easily NRIs can move their money abroad. Here’s a detailed look at their repatriation policies:

NRE Account

Both the principal and interest earned in an NRE account are fully repatriable. NRIs can transfer funds abroad without restrictions or prior approval from the Reserve Bank of India (RBI). Since only foreign income is deposited into this account, there are no repatriation limits, making it a flexible option for global transactions.

NRO Account

Repatriation from an NRO account is subject to restrictions. NRIs can transfer up to USD 1 million per financial year after paying applicable taxes. The account holder must provide necessary documentation, including Form 15CA and Form 15CB, certified by a Chartered Accountant. These rules ensure compliance with Indian tax laws before funds are moved abroad.

How to Open an NRE or NRO Account

NRIs can open an NRE or NRO account through banks and financial marketplace. The process usually requires:

- Proof of NRI status (Passport & Visa/OCI Card)

- Overseas and Indian address proof

- Initial deposit (as per bank requirement)

:

https://in.pinterest.com/jainricha910/

:

https://in.pinterest.com/jainricha910/